Syrup Finance - How to Earn 10%+ on your Dollar Savings

Why your regular bank account will become obsolete.

Most people still save their money in a regular bank (checking- or savings) account. As long as the money is sitting in the bank account, the bank makes use of that capital by lending it out to individuals, companies, or governments. The borrowers (individuals, companies & governments) repay the loan + interest at a rate that is set by the bank. The banks pass on part of that interest to its lenders that provided their money aka. You and pocket the rest for their services.

As an example, I will provide the current interest rates for the Euro (EUR), the British Pound (GBP) & the US Dollar (USD) that you can earn on your account balance on WISE:

4.11% per year - USD

2.45% per year - EUR

3.99% per year - GBP

While these rates may seem like “free money” and “better than nothing” they hardly, if at all will increase your capital and bring you ahead in your financial life. It gets even worse if you adjust these saving rates with the yearly price increase (inflation) in goods and services that you want to buy with your money. The current inflation rates for the above-mentioned currencies at the time of writing (19th of March, 2025) are:

which means if you deduct your bank account earnings from purchasing devaluation your are getting a real yield of:

4,11% - 1,72% = 2.39% in USD

2,45% - 2,5% = -0.05% in EUR

3.99% - 2.60% = 1.39% in GBP

While you are barely beating the current inflation rate in USD and GBP you are even losing purchasing power in EUR. Note that I chose WISE as a favourable example here most banks pass on substantially lower or no rates on to their customers. This is definitely not the way to get ahead in life financially, but what is the alternative?

Savings Rates in Crypto

Shown below are the current (March 19th, 2025) saving rates for USD on the most reputable Crypto lending markets (banks) on Ethereum:

Which leads to a real yield (money that you actually gain!) of:

AAVE: 5,37% - 1.72% = 3,65% in USD

SKY 6.5% - 1.72% = 4,78% in USD

SYRUP 7% - 1.72% = 5,28% in USD

So why is it the case that you can earn between 1.45% - 3,08% more on your USD savings on Ethereum than your regular bank account?

The shortened and simplified answer is, that there are fewer Dollars on Ethereum than in the traditional banking system and the demand relative to the supply is higher on Ethereum than in the bank. That means borrowers are willing to pay more for every dollar that is lent on Ethereum as in the banking system.

To illustrate that this is a consistent phenomenon, look at the historical yields of the above mentioned lending markets in 2024.

The Graph shows:

AAVE: 6.5%

SKY (Sparks sDAI): 7.5%

SYRUP: 11%

If we deduct inflation the inflation rate of last year, which was roughly 3%, we are getting a real yield in 2024 for:

AAVE: 6.5% -3% = 3.5%

SKY: 7.5% - 3% = 4.5%

SYRUP: 11% - 3% = 8%

Think for a second, if you got these yields for the money in the bank account last year.

SYRUP Finance

Now that we know that you can get more for our money on Ethereum, you may ask yourself should I put my hard-earned dollars to earn the best rate for the lowest possible risk?

As you have seen, the current rates are highest in Syrup.fi with 7% in pure USDC yield and even 11.8% if you include the average drip rewards, which are additional tokens given out as incentives to savers. Out of the 3 lending protocols presented Syrup Finance had the highest rates in 2024 with 11% on average (shown in the graphic above). It also had the lowest volatility in rates as shown in the graph below.

While AAVE and Sky saving rates have temporarily fallen to or below 5%, the rate for Syrup Finance was never below 9%. But this sounds too good to be true. You are getting consistently the highest yields with the lowest volatility? How is that possible? The short answer: Syrup is a gateway to Maple which specializes in overcollateralized short-term fixed-rate loans for institutions.

Traditional Lending Market Design

Traditional lending markets like Aave and Sky (to less of an extend) are dependent on the day-to-day supply and demand of Dollar in the Ethereum Economy. Lenders (aka. savers) can provide and redeem any time their money. As can the people that are borrowing the money ask for more or pay back their outstanding loans.

The amount of all saver’s Dollars provided to a lending market divided by the number of Dollars that has been borrowed is called the utilization rate. This rate determines the interest rate that you earn at any given moment. Since Cypto is a very volatile and cyclical industry, rates can be very high one day (usually because prices go up and people want to buy more) and very low the next (usually, because prices do not move for a sustained period or are going down).

Maple Finance- Institutional Lending

While AAVE and Sky are totally permissionless and open markets, where anybody can participate on the lending and borrowing side, Maple Finance is a company that specializes in institutional lending & borrowing. Maple lends the provided money of verified accredited investors only to registered and approved institutions. These loans are overcollateralized meaning for every 1$ that is borrowed, 1.50$ has to be provided in highly liquid crypto assets (usually BTC and ETH) as insurance in case of a default. The loans are given out to these institutions on a previously agreed interest rate and a fixed amount of time, usually between 2 and 30 days. This has three main advantages for the institution:

Unlocking additional Capital to generate income

Why would someone borrow money, when they have to provide even more money to insure said borrow?

Parties that typically borrow from Maple are Market Makers, Exchanges, Hedge Funds, etc. These parties provide BTC & ETH because they think long term these assets will gain in value. At the same time, they might have identified trading/market-making strategies that yield them a higher return than the borrow rate that they are paying. If you could borrow 100$ at 10% for 1 year and you earn 20% on that money during the year you made 10$ in profit. With this money, you can buy even more BTC & ETH. That is essentially what these institutions are doing.

Regulatory Clarity

While it is great for individuals to have open, permissionless markets, in some cases institutions need a trusted intermediary (Maple Finance - the company) to access crypto capital in order to adhere to third-party obligations, such as partners, customers, state-- or federal legislation, etc. Or they just want to hold someone liable in case something goes wrong with their capital.

Financial predictability

The fixed rates allow them to plan as a business, as opposed to when they borrow capital from the open Market (AAVE, etc.) rates may spike within a couple of hours which deems their profit strategy unprofitable. Imagine you have identified a reliable strategy with which you can earn 20% on your borrowed money over the next 20 days. You take out a loan from AAVE for 7%. After 3 days the market starts to move 20% up, and the demand for dollars on AAVE is increasing rapidly which lets the borrow rate go to 21%. All of the sudden you are losing money with your 20% yield strategy. This will not happen on Maple, since institutions can lock in fixed term rates.

For these advantages institutions are willing to pay higher rates than they could get on an open lending market. In addition to the higher borrowing rates that institutions are willing to pay, Maple can send the collateral of its borrowers to work (stake the ETH, etc.) and pass part of this yield to its savers as well. This is possible because of the fixed period that is agreed upon between the borrower and Maple. In the contrary his model does not work for traditional lending markets because borrowers might want to claim back their collateral at any time in kind (ETH for ETH and not sETH). Further, the fixed period (2-30 days) makes the rates for savers less volatile.

Risks

The main risks are:

Smart Contract Risk

The money that you lent to someone over Syrup is secured through a contract (an agreement between you, Maple Finance, and the borrower). You have to sign this contract before you can lend out the money. In the pen & paper world contracts only define rights and obligations with words and have to be enforced by humans with actions. But the contract that you are signing with Maple is not on paper but on a blockchain and instead of words it is written in computer language (code). Code lets the contract not only define the rights and obligations of all parties but also enforce them. This means the contract takes care of your money makes sure it gets into the right hands & is paid back in time, etc. Because the contract on the blockchain has additional capabilities to the one on paper it thinks it is, smart (smart contract).

The smart contracts of Maple have over 686 million Dollars in them. So some people think “I am even smarter than the smart contract and I can trick it into giving me all the money that it holds”. These people are called hackers and they are trying all sorts of strategies to break the logic of the smart contract as people used try to break into physical banks. So how safe are the smart contracts of Syrup & Maple?

Since the crypto space is still young, it is still not very easy to answer this question although some best practices and indicators have been developed over the last year.

Time without hack

Also referred to as the “Lindy effect”. It defines the time period that the protocol has held a significant amount of money without being exploited. Maple contracts have been live since 2021, have facilitated over $6.2B+ loans and there has never been an incident.

Audits

Audits are third-party reviews from specialized cybersecurity firms trying to identify weaknesses. The Maple Finance protocol has undergone 7+ audits, all of which can be found here. These audits have been completed by top-tier firms like Spearbit/Cantina, Three Sigma, and 0xMacro. Additionally, the Syrup Protocol’s main contract, the Syrup Router, has undergone an audit by Three Sigma.

Are the Smart Contract of Maple and Syrup safe?

From a smart contract perspective, the Maple Smart Contracts are as safe as they can be. The 4+ years of years without incident and the high quality of audits make it one of the safest protocols in crypto. Keeping that in mind, there will always be tail risks.

Default on Debt

The second risk is that someone borrows your money and then does not pay it back. This could be happening either because the borrower lost the money or wants to steal it.

Two things should prevent this from happening:

Borrowers Risk Assessment

The Maple Team is vetting every borrower on the most important risk metrics such as their reputation, the total amount of assets held, if they can meet the legal requirements etc.

Overcollaterlized Loans

Vetting the borrowers is a good first step but even the best screening processes could miss some bad apples or the most reliable borrower could find himself unable to pay back loans under unforeseen circumstances. That is why all borrowers have to over-collateralize their loans. This means if they want to borrow 100$ they have to pledge at least 150$ in Bitcoin, Ethereum, or other liquid crypto assets as security (collateral) so that borrowers can be made whole under any circumstances. If the value of their collateral drops to 120$ they will get a “margin called” meaning they have to fill it up until it hits 150$ again. If they fail to do so and the value of collateral drops even further, Maple will liquidate these assets meaning swap their BTC & ETH to dollars and give savers back their money.

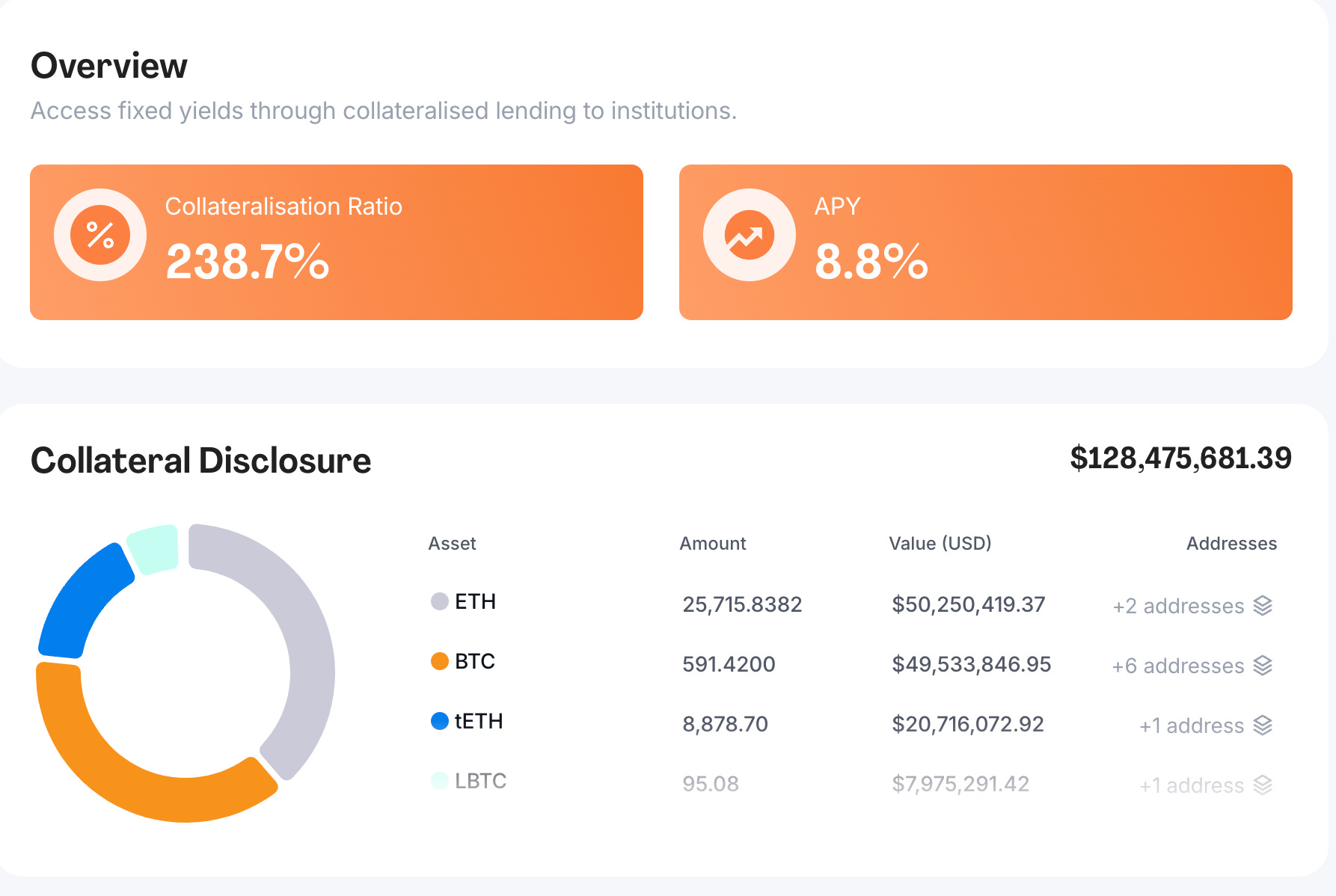

All the assets, that have been posted as collateral are for anyone visibly documented on their website and can be verified through the Ethereum blockchain. As you can see in the figure below the Collateralisation ratio is currently at 238% meaning there are more than double the assets posted as savers insurance as loans outstanding (in Dollar value).

Conclusion

Syrup has identified a very profitable niche in the crypto lending market space. They issue short-term overcollateralized loans to institutions for fixed rates. These institutions are getting regulatory-compliant and predictable market exposure to debt that they can earn profits on. Lenders have higher and more predictable interest rates than on competitive platforms.

Are these the highest rates you can earn if you put your Dollar savings to work in crypto? No, there are higher returns possible. The problem is, that these higher return options are in most cases either, limited in time, bear higher complexity, and/or are associated with additional/higher risks. The goal of the article is to inform crypto beginners that crypto can be an alternative to save your money, which would be otherwise stuck in a bank account.

Syrup finance is one of the easiest, most convenient, and secure ways to get one of the best risk-adjusted returns on your dollar savings in Crypto.